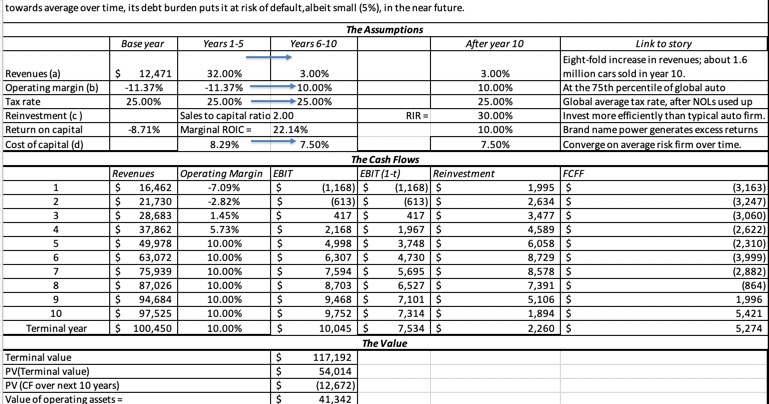

As James Kirk and I have said in recent posts and Andrew said previously, there is a huge absence in numbers in Brendan's posts. [Sorry to personalise this Brendan - it's simply intended in the spirit of debate, etc.]

It seems to me that Brendan's line is that Tesla is overvalued because the price is too high and variations thereof. It may very well be true that it's overvalued - I simply don't know and haven't done any serious research into it.

Yesterday, I put into google: "Tesla earnings estimates" and the first link to appear was this -

I am making no claims that this is a particularly good link. Nonetheless, we have to start somewhere. Anyway, this link provides the consensus earnings estimates (EPS forecasts) for the years ending 2020, 2021 and 2022 from some analysts.

If the consensus estimates are broadly correct, then you can see how the current price is justifiable and that when Tesla's price was circa $300, it wasn't crazily overpriced as has been suggested.

It follows that Brendan must feel that the earnings estimates are seriously wrong. All I would like to know is:

- why does Brendan believe this

- what earnings level does Brendan anticipate over the next few years

I genuinely would like to know!

[All that said - even if Brendan's financial argument is compelling, I'm really not sure if I'd personally be able to get on the shorting Tesla bandwagon. I am too concerned with climate change to hope for poor outcomes for a company which has done so much to raise the bar for EVs.]