You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Referendum on EU budget deal

- Thread starter Shawady

- Start date

While I am not a politician or a party member (out of principle) I am against the referendum passing AND I am not a communist ;-)At the moment I'm planning to vote Yes for the following reasons:

I think this will force the government of the day to limit what is spent based on what it takes in in taxes. I see a lot of extra taxes coming in this year and next, but before long a marginal rate of return will be hit and government spending rather than tax increases will be targetted more.

If we vote No, then IMO that's it - no second go with sweetener thrown in as the pact has already been ratified. All bets are off and we're on our own...and the markets call all of the shots.

The politicians/parties against it appear to be the usual communists.

I see where your line of arguing is coming from, but I don’t think that passing the referendum and letting the EU meddle more in the finances of countries will change anything. What this country needs is to balance the books to 0% deficit spending at the very least, and default on debt. The way I see it that will only happen if access to more debt is turned off. What the new EU legislation will do is allow deficit spending of 3% and pile on more debt.

This is an excellent post, if we were to offer parallels with history which are precarious at best for many reasons, but for the sake of analogy 2008 would be 1929 in the US Great Depression therefore making 2012 the year 1933 and the beginning of FDR's presidency heralding the beginning of the New Deal and vast public works and an attempt to get people back to work and give hope to a nation scarred by four years of depression, unfortunately we do not have an FDR or any attempt to give hope for the future, so I do think the government will have an major task to convince a defeated nation to endorse this treaty.

What FDR and his predecessor Hoover did was take a depression that started in 1929 and make it a Great Depression. Neither FDR, nor WWII ended the depression. What ended the depression was the reduction in government spending and taxation AFTER WWII, which took government out of the way of the private economy.FDR’s new deal probably did more harm than good. The Second World War ended the depression.

Add to that the fact that Ireland has a small and very open economy, unlike the USA in the 1930’s, and injecting money into the economy will see most of that cash leave the country as we buy imported consumer goods. A consumer stimulus package for Ireland is a very bad idea for the same reasons.

Thank god we don’t have an FDR.

Incorrect to say the New Deal did more harm than good, Whether the New Deal was a success or not, depends on the definition of success. That a president, FDR, was actually doing something positive was a huge boost to the American public - they were not being left to fend for themselves,

In 1933 the year Roosevelt took office as president - there were significant improvements. Economic strength and development thrives on confidence and figures give the clear impression that the US had greater confidence in her economic ability after the Crash of 1929. For GDP - this is usually taken as key pointer in a nation's economic health - 1933 to 1939 witnessed a 60% increase; the amount of consumer products bought increased by 40% while private investment in industry increased by 5 times in just six years.

FDR was the president who included in his policies the people who had felt excluded by politics once the Depression had taken its hold. Now the excluded were the included. FDR for me was always just carrying on the policies of former New York Mayor Al Smith, a kinda of hero of mine if it be known!!

This is complete revisionist history. Let’s look at some facts.

1) Unemployment in 1934 was 21.7% and all the government intervention and spending under FDR resulted in a reduction in unemployment to 19% in 1938. Unemployment only went down after millions of American’s were drafted and sent to war

2) FDR paid farmers to destroy crops and live stock to increase prices, while at the same time people were starving

3) Deficit spending was out of control, never had so much government debt been accumulated in peace times, and never had a recession or depression lasted so long

4) GDP went from just under $70bn in 1933 to $85bn in 1938, and all that increase was government spending not private. Private people and organisations were either taxed to the hilt or broke.

Now compare the Great Depression to the depression of 1921, where GDP plummeted, unemployment went through the rough, and in response taxes AND spending were slashed. And it took just 18 months to get out of that depression, as opposed to 17 years for the Great Depression. What is happening now in the western world is exactly the same as what happened in the Great Depression, just to varying degrees and with a lot more debt and money printing.

I suggest you read the following:

http://mises.org/daily/3515

http://www.amazon.co.uk/New-Deal-Raw-Economic-Damaged/dp/1416592229

While I am not a politician or a party member (out of principle) I am against the referendum passing AND I am not a communist ;-)

We all know your a closet commie!

I see where your line of arguing is coming from, but I don’t think that passing the referendum and letting the EU meddle more in the finances of countries will change anything. What this country needs is to balance the books to 0% deficit spending at the very least, and default on debt. The way I see it that will only happen if access to more debt is turned off. What the new EU legislation will do is allow deficit spending of 3% and pile on more debt.

Whatever about defaulting on our debt, balancing our books is impossible to achieve IMO unless there is legislation forcing the government of the day to do so. Otherwise, even with the best intention in the world, politicians will over-spend. At least with this referendum we are closer to tying their hands as it were.

What galls me most, is politicians syaing we need these cuts "so we can go back to the markets" as if this was some sort of goal or achievement! They should really be saying that we need to make these cuts "so we don't have to go back to the markets". Have they learnt nothing?

The fical compact makes no sense in that it does not provide for a government to engage in countercyclical measures.

Think of all the implications:

1) Can't run a deficit above 0.5% - This might be a good aim, but in practice if we had done this in 2008 - 2011 the country would be a basket case now in terms of the real impact on people's lives rather than being simply a financial basket case. It also means we'll probably need another €5bn in austerity measure after the current program.

2) Must reduce debt above 60% by 1/20 per annum. Doesn't this mean we'll need to start repaying about 5bn p.a. off our debts? So the €5bn of austerity measures required after the current program immediately doubles to €10bn.

3) Fining those in financial difficulties? A ridiculous sanction

Bottom line is that you can't run a country without substantial leeway for correcting deficits which will inevitable arise in a global slowdown.

This compact, even with perfect hindsight, does not even address why we got into trouble. A more sensible treaty might focus on restricting spending growth in times when tax revenues are soaring and using the resultant surpluses to run deficits when economies slow down.

People who have been against bank guarantees, austerity, etc should obviously not vote for this.

People who have been in favour of government action taken to date should not vote for it either. Why? The only good argument for the current course of action was that it provided us with money for the day to day running of the country. If we had been able to balance our books immediately in 2008-2010 and didn't need additional money to fund public services, where was the incentive not to default on bank debts, etc?

The fiscal pact contains the following rules:

Think of all the implications:

1) Can't run a deficit above 0.5% - This might be a good aim, but in practice if we had done this in 2008 - 2011 the country would be a basket case now in terms of the real impact on people's lives rather than being simply a financial basket case. It also means we'll probably need another €5bn in austerity measure after the current program.

2) Must reduce debt above 60% by 1/20 per annum. Doesn't this mean we'll need to start repaying about 5bn p.a. off our debts? So the €5bn of austerity measures required after the current program immediately doubles to €10bn.

3) Fining those in financial difficulties? A ridiculous sanction

Bottom line is that you can't run a country without substantial leeway for correcting deficits which will inevitable arise in a global slowdown.

This compact, even with perfect hindsight, does not even address why we got into trouble. A more sensible treaty might focus on restricting spending growth in times when tax revenues are soaring and using the resultant surpluses to run deficits when economies slow down.

People who have been against bank guarantees, austerity, etc should obviously not vote for this.

People who have been in favour of government action taken to date should not vote for it either. Why? The only good argument for the current course of action was that it provided us with money for the day to day running of the country. If we had been able to balance our books immediately in 2008-2010 and didn't need additional money to fund public services, where was the incentive not to default on bank debts, etc?

The fiscal pact contains the following rules:

- General government budgets shall be balanced or in surplus. The annual structural deficit must not exceed 0.5% of nominal GDP. Countries with government debt levels significantly below 60 % and where risks in terms of long-term sustainability of public finances are low, can reach a structural deficit of at most 1.0 % of GDP.

- Member States whose government debt exceeds the 60% reference level shall reduce it at an average rate of one twentieth per year as a benchmark.

- EU's highest court will be able to fine a country that does not adopt a standardised balanced budget rule in its constitution - with a penalty equivalent to up to 0.1% of GDP.

Duke of Marmalade

Registered User

- Messages

- 4,716

DerKaiser

The 0.5% restriction is on structural deficit. This is a very flexible concept and really allows great scope for interpretation. Ireland's deficits in recent years are clearly largely cyclical, with unemployment in the teens.

The glidepath of 1/20th of the excess over 60% applies to the excess not the debt and has been shown by Colm McCarthy to be largely irrelevant should we get a balanced budget by 2016. Nominal growth would mean that we would comfortably meet the glidepath with a zero deficit, you only need 2% nominal growth to be on target for the glidepath if say the Debt was 100% of GDP. (1/20th x (100 - 60) = 2).

I have read this Treaty. It is largely aspirational just like the Stability and Growth Pact before it. Almost every country is currently in "breach" (Germany's debt/GDP ratio is 80%). There are so many outs like use of the term "structural", or "medium term objectives" or "in exceptional circumstances". This is purely a political exercise with all the naughty children renewing their vows and promising to behave at some time in the future - Lord may I give up sin, but not just yet!

Anybody who votes against this as a way of thumbing our noses at the EU establishment or the Germans or even our own government needs their head examined.

The 0.5% restriction is on structural deficit. This is a very flexible concept and really allows great scope for interpretation. Ireland's deficits in recent years are clearly largely cyclical, with unemployment in the teens.

The glidepath of 1/20th of the excess over 60% applies to the excess not the debt and has been shown by Colm McCarthy to be largely irrelevant should we get a balanced budget by 2016. Nominal growth would mean that we would comfortably meet the glidepath with a zero deficit, you only need 2% nominal growth to be on target for the glidepath if say the Debt was 100% of GDP. (1/20th x (100 - 60) = 2).

I have read this Treaty. It is largely aspirational just like the Stability and Growth Pact before it. Almost every country is currently in "breach" (Germany's debt/GDP ratio is 80%). There are so many outs like use of the term "structural", or "medium term objectives" or "in exceptional circumstances". This is purely a political exercise with all the naughty children renewing their vows and promising to behave at some time in the future - Lord may I give up sin, but not just yet!

Anybody who votes against this as a way of thumbing our noses at the EU establishment or the Germans or even our own government needs their head examined.

I'd be worried about the flip side, where we feel we can't oppose it for fear of losing EU support even if the treaty might not make sense as a means in itself.Anybody who votes against this as a way of thumbing our noses at the EU establishment or the Germans or even our own government needs their head examined.

SeamusCoffey

Registered User

- Messages

- 29

Double post

SeamusCoffey

Registered User

- Messages

- 29

The fical compact makes no sense in that it does not provide for a government to engage in countercyclical measures.

Think of all the implications:

1) Can't run a deficit above 0.5% - This might be a good aim, but in practice if we had done this in 2008 - 2011 the country would be a basket case now in terms of the real impact on people's lives rather than being simply a financial basket case. It also means we'll probably need another €5bn in austerity measure after the current program.

No, a country can't run a structural deficit of more than 0.5% of GDP (or 1.0% of if it below the 60% of GDP debt threshold). There is still scope for cyclical deficits. Structural deficits must be created, i.e. they are based on political decisions to increase expenditure and/or cut taxes. Cyclical deficits just happen. In a downturn tax revenues fall and social welfare expenditure rises without any political decisions. This cyclical element is still allowed. The constraints are being put on deficits created by decisions.

Of course, telling what part of the deficit is due to the economic cycle and what part is due to political decisions is a whole different matter but the statement above is wrong. There is more here.

2) Must reduce debt above 60% by 1/20 per annum. Doesn't this mean we'll need to start repaying about 5bn p.a. off our debts? So the €5bn of austerity measures required after the current program immediately doubles to €10bn.

This is also very much wrong but has been stated so often by opposition politicians and many commentators that one could easily think it is true. It is not. The rule is not to force countries to start repaying debt merely to get them to slow down the accumulation of debt. It is a debt brake not a debt reverse.

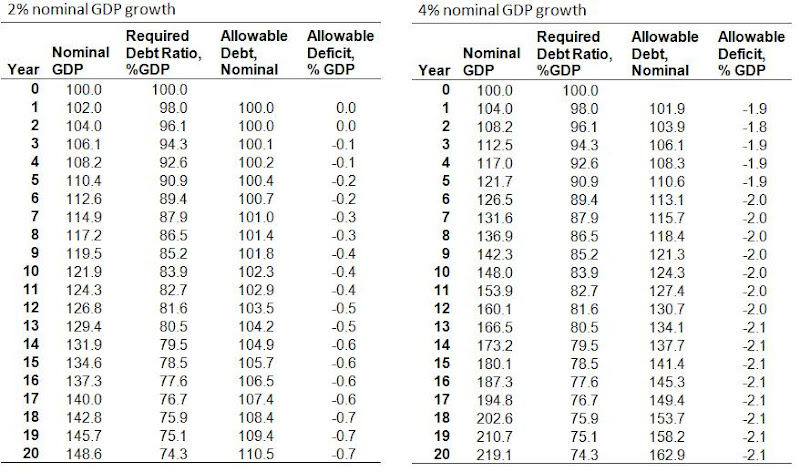

Here is an approximate 20-year pattern for a country with a starting debt of 100% of GDP (with GDP set to 100 for simplicity) under two growth scenarios, 2% and 4% nominal GDP growth scenarios. For what it's worth Irish nominal GDP growth averaged 11.5% from 1971 to 2010 but the conditions are completely different now.

You can see that the nominal debt never declines and there are only two years of a balanced budget required under the low-growth 2% scenario before the country can resume deficits and borrowing under the debt brake rule. 2% is the ECB's inflation target so this is akin to no real growth. With 4% nominal growth the country can run continual deficits of 2% of GDP and satisfy the rule. Again more here.

3) Fining those in financial difficulties? A ridiculous sanction

No, the countries that may be fined will be those who break the rules and don't do anything to address it. There is huge room for manoeuvre built into the provisions, "exceptional circumstances", "significant downturn" etc.

Bottom line is that you can't run a country without substantial leeway for correcting deficits which will inevitable arise in a global slowdown.

This compact, even with perfect hindsight, does not even address why we got into trouble. A more sensible treaty might focus on restricting spending growth in times when tax revenues are soaring and using the resultant surpluses to run deficits when economies slow down.

There is leeway for cyclical deficits that arise in a slowdown. The whole point is to stop politically created ones. There is an expenditure rule in the revised Stability and Growth Pact. The debt and deficit rules would had no impact in Ireland between 2000 and 2007 but the new expenditure rule would have.

People who have been against bank guarantees, austerity, etc should obviously not vote for this.

The treaty has absolutely nothing to do with bank guarantees and very little to do with the austerity in Ireland. Regardless of whether this treaty is passed or not we still have to bring the annual deficit under control. The provisions in the treaty will not have a direct effect in Ireland until three years after we leave the Excessive Deficit Procedure. That is not due to happen until 2015 so the rules become effective in 2018. If we are still running massive deficits then we are goosed.

Duke of Marmalade

Registered User

- Messages

- 4,716

Seamus

Whilst you talk too much sense to ever qualify as a "celebrity economist" you are nonetheless most welcome to AAM.

I made somewhat similar comments on DerKaiser's post though not so eloquently as yourself and not on the double.

A couple of observations on the math:

(a) The debt brake, if only it applied, would mean that a Debt/GDP ratio of X% (>60%) would be 60%+.95^n x (X-60)% after n years i.e. it would never reach 60% as indeed your spreadsheets show after 20 years.

(b) If the balanced budget applies then the Debt/GDP ratio will reduce each year by the nominal rate of growth i.e. will always reduce even when below the "safe" 60%. So, ignoring cyclical effects, a balanced budget is in fact an aspiration to trend the Debt/GDP ratio towards zero. Am I interpreting that correctly and does that make economic sense? Would a target of 60% not be more conducive to growth and continued investment in State infrastructure?

Whilst you talk too much sense to ever qualify as a "celebrity economist" you are nonetheless most welcome to AAM.

I made somewhat similar comments on DerKaiser's post though not so eloquently as yourself and not on the double.

A couple of observations on the math:

(a) The debt brake, if only it applied, would mean that a Debt/GDP ratio of X% (>60%) would be 60%+.95^n x (X-60)% after n years i.e. it would never reach 60% as indeed your spreadsheets show after 20 years.

(b) If the balanced budget applies then the Debt/GDP ratio will reduce each year by the nominal rate of growth i.e. will always reduce even when below the "safe" 60%. So, ignoring cyclical effects, a balanced budget is in fact an aspiration to trend the Debt/GDP ratio towards zero. Am I interpreting that correctly and does that make economic sense? Would a target of 60% not be more conducive to growth and continued investment in State infrastructure?

There's a lot of fair points being made.

I would agree that we should be running balanced budgets anyway within a few years (if not, we are in worse trouble than we thought - if that is possible!)

Fair enough about there being leeway to define structural deficits or to run them in exceptional circumstances.

Fair enough that growth in GDP might eliminate the need to actually reduce nominal outstanding debt. From what I have seen, our national debt will certainly peak above 120% GDP, requiring GDP growth of 3% in each year to avoid paying down debt. Again, like balancing the budgets, I'd agree that eroding the real value of the debt without necessarily paying it down is where we'd want to be.

In summary we would like to balance our budgets and not rack up any more debt by say 2015/2016 and that might tie in with the constraints of the compact. But what if we don't quite balance the books or if we get lower growth than 3%?

And what if, a bit further down the road, tax revenues slumped by 30% again over a 2 year period (as in 2007 to 2009)? Would structural deficit calculations genuinely allow us to avoid an immediate €15bn in spending cuts? I'm not convinced. Was our structural deficit in 2011 far less than that of 2007 following 3/4 years of austerity? If not, I really don't see how structural deficits make allowance for appropriate behaviours.

I would agree that we should be running balanced budgets anyway within a few years (if not, we are in worse trouble than we thought - if that is possible!)

Fair enough about there being leeway to define structural deficits or to run them in exceptional circumstances.

Fair enough that growth in GDP might eliminate the need to actually reduce nominal outstanding debt. From what I have seen, our national debt will certainly peak above 120% GDP, requiring GDP growth of 3% in each year to avoid paying down debt. Again, like balancing the budgets, I'd agree that eroding the real value of the debt without necessarily paying it down is where we'd want to be.

In summary we would like to balance our budgets and not rack up any more debt by say 2015/2016 and that might tie in with the constraints of the compact. But what if we don't quite balance the books or if we get lower growth than 3%?

And what if, a bit further down the road, tax revenues slumped by 30% again over a 2 year period (as in 2007 to 2009)? Would structural deficit calculations genuinely allow us to avoid an immediate €15bn in spending cuts? I'm not convinced. Was our structural deficit in 2011 far less than that of 2007 following 3/4 years of austerity? If not, I really don't see how structural deficits make allowance for appropriate behaviours.

Since the Oireachtas has not yet ratified the ESM Treaty 2 then surely if we were to vote NO then the Oireachtas would not ratify it. They would be ratifying something which our so-called European partners have already said we would not have access to in the event of a NO. Great big turkeys voting for Christmas for all us little turkeys?

Surely a NO then would put the Government of Ireland in a strong position to renegotiate the promissory notes issue since the ESM treaty requires ratification by all 27 countries whereas the Fiscal Compact does not.

So by voting NO you are actually empowering the government even if they themselves are too weak or incompetent to see that yet.

Surely a NO then would put the Government of Ireland in a strong position to renegotiate the promissory notes issue since the ESM treaty requires ratification by all 27 countries whereas the Fiscal Compact does not.

So by voting NO you are actually empowering the government even if they themselves are too weak or incompetent to see that yet.

Hahaha, what's the quote about the greatest trick of the devil?We all know your a closet commie!

I agree, it is politically unpalatable/impossible, which is why I believe a balancing of the books will eventually be forced by the next stages of the financial crisis. And I'm all in favor of a constitutional restriction of precisely 0% deficit.Whatever about defaulting on our debt, balancing our books is impossible to achieve IMO unless there is legislation forcing the government of the day to do so. Otherwise, even with the best intention in the world, politicians will over-spend. At least with this referendum we are closer to tying their hands as it were.

I hear you, it's very frustrating indeed.What galls me most, is politicians syaing we need these cuts "so we can go back to the markets" as if this was some sort of goal or achievement! They should really be saying that we need to make these cuts "so we don't have to go back to the markets". Have they learnt nothing?

If this crisis and the lead up to it has proven anything it is that the economy cannot be controlled top down through some pulling of levers and flipping of switches.The fical compact makes no sense in that it does not provide for a government to engage in countercyclical measures.

That was said about Iceland when it refused to take on the private sector debt and went into default. It was nonsense then and has been proven to be nonsense now. A sharp and fast cutting of spending is exactly what was needed here. Instead we have had a little cutting here, some more bailing out there, and higher taxes to top it off, resulting in much higher debt and still no meaningful reduction in the deficit 4 YEARS later.1) Can't run a deficit above 0.5% - This might be a good aim, but in practice if we had done this in 2008 - 2011 the country would be a basket case now in terms of the real impact on people's lives rather than being simply a financial basket case. It also means we'll probably need another €5bn in austerity measure after the current program.

I agree with the other posts that there is nothing in the treaty that suggests that the amount of outstanding debt will actually be reduced.2) Must reduce debt above 60% by 1/20 per annum. Doesn't this mean we'll need to start repaying about 5bn p.a. off our debts? So the €5bn of austerity measures required after the current program immediately doubles to €10bn.

I agree, especially since there is already a fantastic mechanism to do this, it is called the bond market.3) Fining those in financial difficulties? A ridiculous sanction

Not true, all you need is a reasonably sized buffer of real savings to make up temporary minor shortfalls. The comment reminds of a friend who told me years ago, that you cannot go through life without loans. It is simply not true.Bottom line is that you can't run a country without substantial leeway for correcting deficits which will inevitable arise in a global slowdown.