SuperMario

Registered User

- Messages

- 16

Has it been confirmed if the Switch account is affected by this change? I can't see to find any details from PTSB. The only source seems to be various news articles which are lacking detail

I'm just amused tbh. The absolute hassle of changing banks to stick it to the bank that has given you free banking for 30 years, especially when the free alternatives are pretty much non-existent. Current accounts are actually great value in Ireland.You seem fixated on the word free. They marketed it as free, including the past few years only if you kept a min of €2500 a month in your account. I qualified for free banking, which they offered

I have covered the loyalty matter above. What's so difficult to understand?

If its not free, why should I stay?

It's a measure I hope back fires on them. For every 1 of the estimated 47k legacy free account holders there is also the small matter of the €2500 permanently in deposit at 0.0001% interest at best. That's a potential €117m of interest free money they are putting on the line for a marginal profit.The RTE report includes the words "around 47,000 customers were actively using the fee waiver feature, which is being removed."

If PTSB can manage to hold on to most of those customers, then they'll be earning all of an extra €3m a year. A mere drop in the ocean given their forecast income of €650m in 2023!

I think that I get free banking from them because I'm an OAP, but will be anxiously watching this thread to see whether I'll have to cancel one of my three annual overseas vacations, or, worse still, let one of the servants go!

Fair enough.. In all liklihood they are banking on well documented Irish customer inertia.I'm just amused tbh. The absolute hassle of changing banks to stick it to the bank that has given you free banking for 30 years, especially when the free alternatives are pretty much non-existent. Current accounts are actually great value in Ireland.

It's a measure I hope back fires on them. For every 1 of the estimated 47k legacy free account holders there is also the small matter of the €2500 permanently in deposit at 0.0001% interest at best. That's a potential €117m of interest free money they are putting on the line for a marginal profit.

This is most likely a reaction to having to up interest rates on deposits which are still very low. They had a USP on free banking allowing them to compete with the big two. IMO they are a basket case of an institution that will never learn from their mistakes.

When/where did they say “Free Banking for Life”?

I get that you’re saying that, but your post and an 18 year old letters page from the Indo aren’t conclusive evidence of anything. Where the product literature? Might it be the lifetime of the product rather than the lifetime of the customer?The PTSB Switch Current Account (one of the legacy PTSB current account products which seems unaffected by this announcement) was effectively advertised as free banking for life.

PTSB said that Switch product was a "lifetime" product.

This Irish Independent article from 2005 makes reference to the "lifetime" aspect.

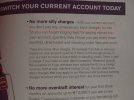

That does seem worthy of escalating to be fair. They could try to argue that monthly fees are okay whereas quarterly ones aren’t, but that would be pretty disingenuous.I was wondering if anyone had the Switch brochure. Not sure if the attachment will work here, but my copy says “no more silly charges - with our current account, you don’t pay any unnecessary charges for life!” And goes on to state the kind of fees you won’t have to pay.

That does seem worthy of escalating to be fair. They could try to argue that monthly fees are okay whereas quarterly ones aren’t, but that would be pretty disingenuous.

"you don't pay any unnecessary charges.." I guess they could just say that charges have become necessaryI was wondering if anyone had the Switch brochure. Not sure if the attachment will work here, but my copy says “no more silly charges - with our current account, you don’t pay any unnecessary charges for life!” And goes on to state the kind of fees you won’t have to pay.

")

On what date will the fees waver end?Got a letter today from permanent tsb re the ending of the €2500 fee waiver feature.