podgerodge

Registered User

- Messages

- 1,062

I don't want to de-rail the main Bunq interest thread, so starting this specifically to discuss (if anyone can) the difference between the "Joint Savings Account", which I think is a "sub-account" with the 1.56% interest, and a "Joint Account" - which I'm not sure about at all.

With any savings over €100k, it's obviously extremely important that the legal ownership is clear - for deposit protection purposes given 100k limit per person.

I have 1 "Joint Savings Account" set up with my wife 'invited' to access the account. I wanted to know whether we are both legal owners as above or whether, as some Bunq material suggests, she was just an add-on with access to the account to transact, but not a "co-owner". (Incidentally, I don't see "co-owner" anywhere on my app or the web interface".

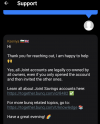

So, I asked Bunq. They responded: "Yes, all Joint accounts are legally co-owned by all owners, even if you only opened the account and then invited the other ones - Learn all about Joint Savings accounts here...........(link)" - NOTE - that they say "all joint accounts", not "all joint savings accounts" - you'd assume they are the same - but see further down below about converting one to the other.

I would have been happy that everything was all in order with that response, other than that at the link they provided above, it states:

"If you experience any difficulties withdrawing funds from your Joint Savings Account or you want faster access to your savings - you can convert one of your Joint Savings Accounts into a regular Joint Account! It's easy....."

I have no idea why there would be "difficulties" withdrawing funds from a joint savings account, or what "faster access to my savings" means, but have no idea what the difference between the 2 is - and again, whether there are legal differences in ownership between the 2 types of account. I suspect that Bunq are using poor terminology and that a "regular" Joint Account is deemed to be some type of current account that doesn't attract interest. But can't find anything to support this.

I might ask Bunq to tell me what the difference is!

Anyway, this is just in case other people have similar questions, or indeed, have joint accounts but haven't thought about the differences. It's reasonable to make sure that you are 100% sure of the legal position, and Bunq aren't making that easy. I will update when I get a response.

With any savings over €100k, it's obviously extremely important that the legal ownership is clear - for deposit protection purposes given 100k limit per person.

I have 1 "Joint Savings Account" set up with my wife 'invited' to access the account. I wanted to know whether we are both legal owners as above or whether, as some Bunq material suggests, she was just an add-on with access to the account to transact, but not a "co-owner". (Incidentally, I don't see "co-owner" anywhere on my app or the web interface".

So, I asked Bunq. They responded: "Yes, all Joint accounts are legally co-owned by all owners, even if you only opened the account and then invited the other ones - Learn all about Joint Savings accounts here...........(link)" - NOTE - that they say "all joint accounts", not "all joint savings accounts" - you'd assume they are the same - but see further down below about converting one to the other.

I would have been happy that everything was all in order with that response, other than that at the link they provided above, it states:

"If you experience any difficulties withdrawing funds from your Joint Savings Account or you want faster access to your savings - you can convert one of your Joint Savings Accounts into a regular Joint Account! It's easy....."

I have no idea why there would be "difficulties" withdrawing funds from a joint savings account, or what "faster access to my savings" means, but have no idea what the difference between the 2 is - and again, whether there are legal differences in ownership between the 2 types of account. I suspect that Bunq are using poor terminology and that a "regular" Joint Account is deemed to be some type of current account that doesn't attract interest. But can't find anything to support this.

I might ask Bunq to tell me what the difference is!

Anyway, this is just in case other people have similar questions, or indeed, have joint accounts but haven't thought about the differences. It's reasonable to make sure that you are 100% sure of the legal position, and Bunq aren't making that easy. I will update when I get a response.