BIG-notorious

Registered User

- Messages

- 111

This question has been niggling me for a while.

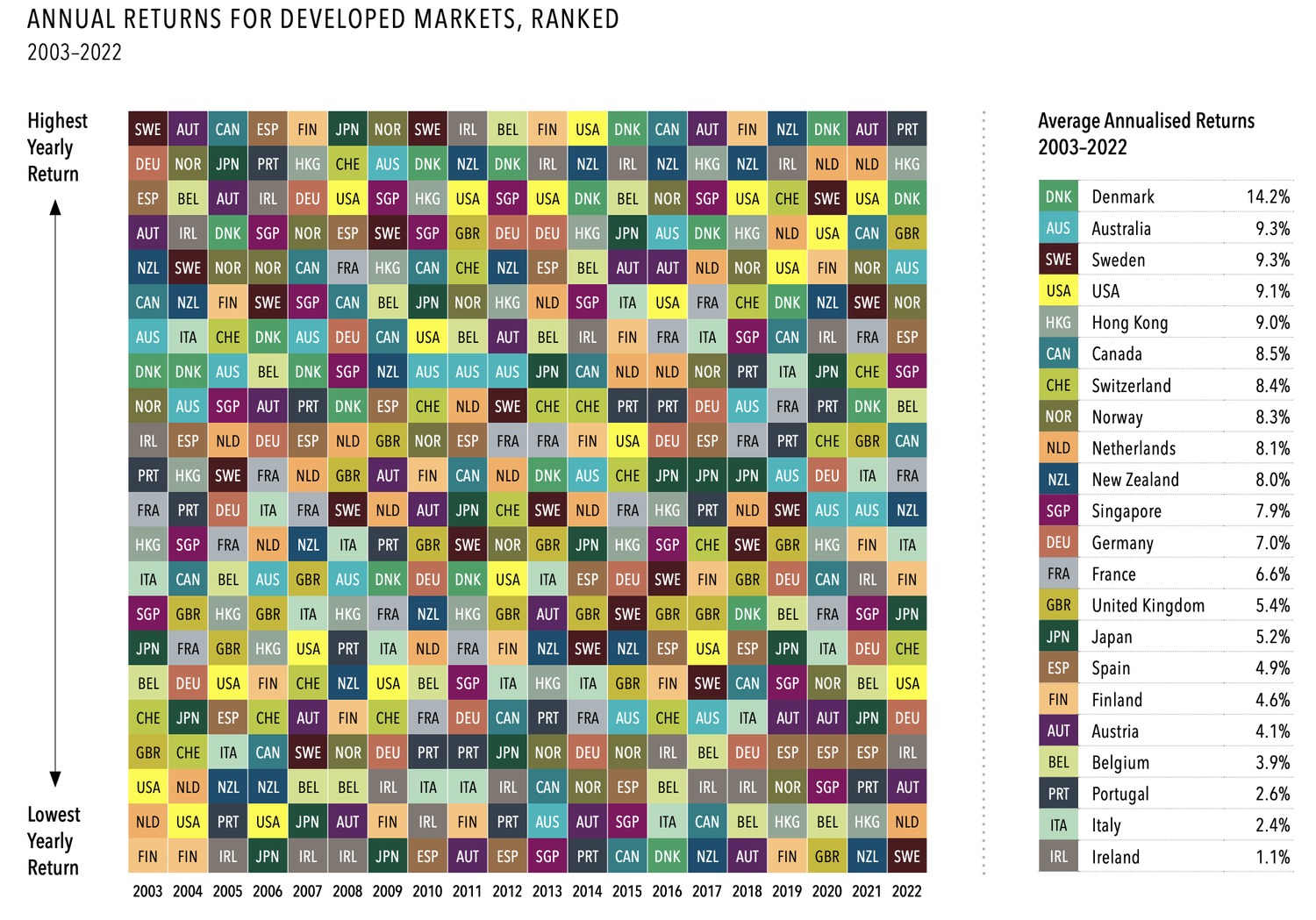

This makes total sense in the short term and also for individual stocks. But for different indices in the long term it seems reasonable to assume that differing performance is based at least partially on differing systems and cultures in their originating regions, as well as that countries commercial focus. Competition & consumer law in the EU (for example) seems to make it unlikely that we could produce megacorps like Google.

It also seems unlikely that a four decade long trend is just random. So why does it make any sense at all to ignore decades of performance? Why act like the Nikkei is just as good as the S&P 500 when the S&P has increased by over 30 times in the last 40 years while the Nikkei has only tripled? Or that a global index is better than the S&P 500 when the S&P performs consistently (if only slightly) better the All World?

Our pensions are for many (certainly myself) their biggest investment decision outside of purchasing their home. But even though we routinely check out the past performance of our cars, homes, restaurants, staff and even our significant others, and then we're told that not only that past performance is not only irrelevant but it's actually dangerous to pay any attention to it when it comes to deciding how our pension should be invested (which again seems like good advice only for relatively short-term investments or individual stocks). Often it's advised to just get the lowest cost global index available.

I'd really like to know why this is. Because honestly it doesn't seem rational to just ignore numbers on long term past performance of indices.

- A few people on my other thread commented to the effect that the last 40 years of comparative performance data was meaningless, and I should just invest in a global index so I'm properly diversified.

- The other day I saw a video on instagram which referenced John Bogle (who I've heard of obviously but haven't read myself) as saying that past performance is a trap and people should just put all their money into the S&P 500.

This makes total sense in the short term and also for individual stocks. But for different indices in the long term it seems reasonable to assume that differing performance is based at least partially on differing systems and cultures in their originating regions, as well as that countries commercial focus. Competition & consumer law in the EU (for example) seems to make it unlikely that we could produce megacorps like Google.

It also seems unlikely that a four decade long trend is just random. So why does it make any sense at all to ignore decades of performance? Why act like the Nikkei is just as good as the S&P 500 when the S&P has increased by over 30 times in the last 40 years while the Nikkei has only tripled? Or that a global index is better than the S&P 500 when the S&P performs consistently (if only slightly) better the All World?

- Worse again seems the notion that the Nikkei is the better bet now because it's underperformed the S&P for so long.

Our pensions are for many (certainly myself) their biggest investment decision outside of purchasing their home. But even though we routinely check out the past performance of our cars, homes, restaurants, staff and even our significant others, and then we're told that not only that past performance is not only irrelevant but it's actually dangerous to pay any attention to it when it comes to deciding how our pension should be invested (which again seems like good advice only for relatively short-term investments or individual stocks). Often it's advised to just get the lowest cost global index available.

I'd really like to know why this is. Because honestly it doesn't seem rational to just ignore numbers on long term past performance of indices.